Skip to content

Skip to content

So you want to start your own business, eh? That choice is not for the faint of heart! In fact, it will require that you learn countless skills that are not the slightest bit related to your business of choice. One such skill is bookkeeping for startups.

Let me tell you a story that’ll make your entrepreneurial heart skip a beat and not in a good way.

I once knew a general contractor who was absolutely crushing it…or so he thought. He had three major renovation projects running simultaneously. His crew was booked solid for months and the checks were rolling in. He figured he had to making money hand over fist but when tax season rolled around, he sat in his accountant’s office with a shoebox of crumpled receipts and a sick feeling in his stomach. Turns out, two of his “profitable” projects were actually bleeding money due to material cost overruns and unpaid change orders. He’d been so busy directing his subs that he didn’t have time to add up his expenses. Without the numbers, he had no idea which jobs were padding his bank account and which ones were sucking it dry.

Welcome to the world of startup bookkeeping—where dreams go to die if you aren’t prepared.

But here’s the thing…I’ve seen brilliant businessmen, with game-changing ideas, crash and burn because they treated bookkeeping like that elliptical machine in their bedroom that is draped with laundry because they never use. And I’ve watched equally passionate entrepreneurs scale their businesses to seven figures because they had their financial records dialed in from day one.

The difference? They understood that bookkeeping for startups isn’t just about keeping Uncle Sam happy, it’s about having the financial intelligence and data to make smart business decisions that help your business succeed.

Why Bookkeeping for Startups Is Your Secret Weapon (Not Your Nemesis)

Let’s get real for a second. When you hear “bookkeeping,” you probably think about dusty ledgers and accountants with thick glasses. But modern startup bookkeeping is more like having a GPS for your business finances. It tells you exactly where you are, where you’re going, and how to avoid those financial potholes that’ll wreck your ride.

Here’s what proper accounting for startups actually does for you:

It turns chaos into clarity. Instead of guessing whether you can afford that new hire or wondering why your bank account is dwindling, you’ll have real data to make real decisions.

It makes investors take you seriously. Nothing says “amateur hour” like showing up to a funding meeting with a box full of receipts. Professional financial records? That’s how you get taken seriously.

It saves your butt during tax season. Trust me, there are few things more stressful than searching through old emails for expense receipts while the IRS auditor taps their foot.

The Foundation: Setting Up Your Startup Accounting System

Separate Business and Personal Finances (Seriously, Do This Today)

This is bookkeeping 101, yet I still see seasoned entrepreneurs mixing their morning Starbucks coffee purchases with business expenses. Here’s why this matters more than you think:

When you mix personal and business finances, you’re not just creating a bookkeeping headache, you’re potentially compromising your legal protection and making tax time a nightmare. Plus, try explaining to an investor why your “marketing expenses” include last weekend’s grocery run.

The fix is simple: Open a dedicated business bank account (I like Grasshopper). Like, right now. Before you finish reading this article. I’ll wait.

Choose Your Accounting Method: Cash vs. Accrual

This sounds boring, but stick with me. This decision affects everything from your tax bill to how you understand your business performance.

Cash accounting is like keeping track of money in your wallet. You record income when you actually receive it and expenses when you actually pay them. It’s simple, straightforward, and perfect for small startups with straightforward transactions.

Accrual accounting is more like tracking promises. You record income when you earn it (even if the check hasn’t arrived) and expenses when you incur them (even if you haven’t paid yet). It gives you a more accurate picture of your business performance but requires more sophisticated tracking.

For most startups, cash accounting is the way to go. That said, if you’re planning to seek significant investment or have complex revenue models you might want to dig a little deeper on this topic because accrual accounting might be more preferential.

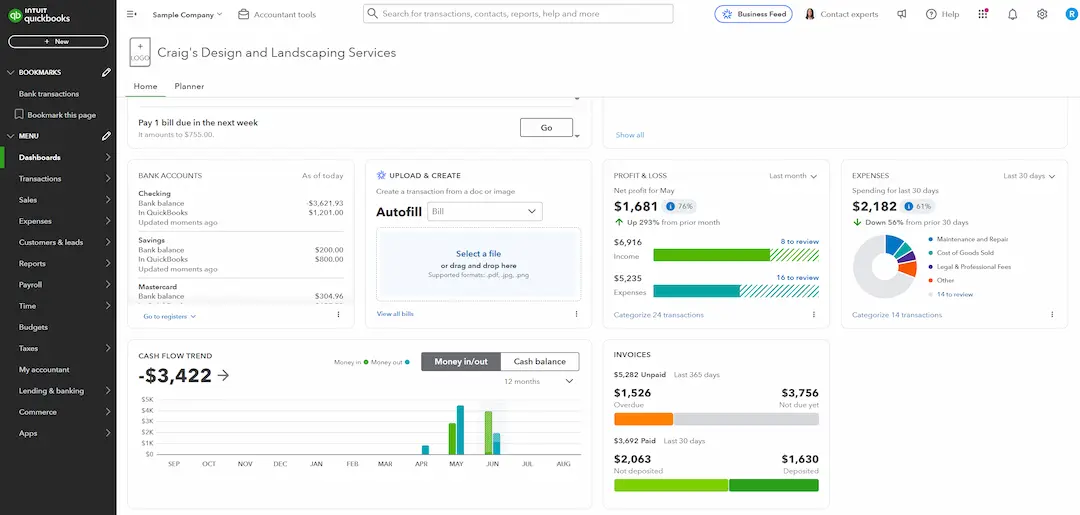

The Best Bookkeeping Software for Startups (And Why You Need It)

Let me save you some time: forget about spreadsheets. I know, I know—Excel feels familiar, and Google Sheets is free. But using spreadsheets for startup accounting is like using a flip phone in 2025. Sure, it technically works, but you’re making life unnecessarily difficult.

Here’s my breakdown of the top bookkeeping software for startups:

| Software | Best For | Price Range | Key Features |

| QuickBooks Online | Most startups | $15-$200/month | Comprehensive features, great integrations, investor-ready reports |

| Xero | International businesses | $13-$70/month | Beautiful interface, strong bank reconciliation, multi-currency support |

| Wave | Bootstrap startups | Free (paid add-ons available) | Completely free core features, perfect for bare-bones needs |

| FreshBooks | Service-based startups | $15-$50/month | Excellent time tracking, client management, invoicing |

My recommendation? Start with QuickBooks Online (QBO). It’s the industry standard, plays nice with other business tools, and gives you room to grow. Plus, when you eventually hire a bookkeeper or accountant, they’ll already know how to use it.

Essential Financial Records Every Startup Must Keep

Think of your financial records as the DNA of your business—they tell the complete story of how your company operates and where it’s headed. Here’s what you absolutely cannot afford to ignore:

Income Tracking

Every dollar that comes into your business needs to be recorded. This includes:

- Sales revenue

- Investment funding

- Loans

- Interest income

- That random refund from your software subscription

Expense Management

If money leaves your business, it gets tracked. Period. This covers:

- Office rent and utilities

- Software subscriptions

- Marketing and advertising costs

- Professional services (legal, accounting, consulting)

- Travel and meals (yes, even that working lunch counts)

- Equipment and supplies

The Receipt Reality Check

Here’s a truth bomb: if you didn’t document it, it didn’t happen (at least according to the IRS). Develop a system for capturing receipts immediately. Whether that’s snapping photos with your phone or using expense-tracking apps, make it automatic.

Managing Cash Flow: The Startup Survival Skill

Cash flow management is where most startups live or die. You can be profitable on paper and still go out of business if you run out of cash. Let me explain this with a scenario that’ll make it crystal clear:

Imagine you just landed a massive contract worth $100,000. Congratulations! But there’s a catch; your client pays net-60 terms, meaning you won’t see that money for two months. Meanwhile, you need to pay your team, cover your rent, and fund the project delivery. Without proper cash flow management, that amazing contract could actually be the death blow to your business.

Cash Flow Forecasting Made Simple

Create a 13-week rolling cash flow forecast. It sounds fancy, but it’s just a simple table showing:

- Week-by-week expected income

- Week-by-week expected expenses

- Your projected cash balance

Update this weekly, and you’ll never be surprised by cash shortages again.

The Most Common Bookkeeping Mistakes (And How to Avoid Them)

I’ve seen these mistakes kill more startups than bad market timing or fierce competition. Learn from others’ pain:

Mistake #1: The “I’ll Do It Later” Trap

Procrastinating on bookkeeping is like procrastinating on exercise—the longer you wait, the more painful it becomes. Set aside time weekly for financial maintenance. Treat it like brushing your teeth. It’s not fun, but absolutely necessary, unless you’re okay with a liquid diet.

Mistake #2: Mixing Personal and Business Expenses

We covered this earlier, but it bears repeating. Keep them separate, always. This one seems unimportant until it’s a big deal, but once you reach that point, it’s difficult and painful to un-ring that bell.

Mistake #3: Ignoring Small Expenses

Those $5 coffee purchases and $10 software subscriptions add up faster than you think. Track everything, no matter how small. This is where a connected bookkeeping software package like QuickBooks Online that automatically downloads your bank feeds comes in handy and also where Excel will really show the kinks in its armor.

Mistake #4: Not Backing Up Financial Data

Your bookkeeping records are more valuable than your laptop. Use cloud-based solutions and regular backups. Losing years of financial data is a business-ending catastrophe.

Tax Compliance for Startups: Staying on the Right Side of the IRS

Nobody starts a business dreaming about tax compliance, but ignoring it is like playing Russian roulette with your company’s future. Here’s how to stay compliant without losing your mind:

Quarterly Tax Payments

If your startup is profitable, you’ll likely need to make quarterly estimated tax payments. Missing these can result in penalties that’ll make your accountant weep.

Expense Deductions

Proper bookkeeping ensures you don’t miss valuable tax deductions by capturing every possible business expense. Common startup deductions include:

- Home office expenses (if you work from home)

- Business meals (50% deductible)

- Software and equipment

- Professional development and education

- Marketing and advertising costs

Sales Tax Considerations

If you sell products or certain services, you might need to collect and remit sales tax. This varies by state and can be complex for online businesses.

When to Hire Professional Help

Here’s the honest truth: trying to do everything yourself isn’t noble and it’s often expensive. I recently reviewed financials for a prospective client that recorded roughly $45,000 worth of deductible expenses as “fixed assets” but did not depreciate them. The result? They overpaid in income tax by more than $14,000. That overpayment would have paid for the bookkeeping services to avoid it multiple times over.

Here’s when you should consider bringing in professional outsourced bookkeeping services for startups:

Hire a bookkeeper when:

- You’re spending more than 5 hours per week on bookkeeping

- You’re consistently behind on financial record-keeping

- You’re making repeated errors or feeling overwhelmed

- You need more time to focus on growing your business

Hire an accountant when:

- You’re raising investment capital

- Your business structure is becoming complex

- You’re dealing with multiple revenue streams

- Tax planning becomes crucial for your growth strategy

The cost of professional help is almost always less than the cost of financial mistakes or missed opportunities.

Leveraging Financial Data for Business Decisions

This is where bookkeeping transforms from a necessary evil into your business superpower. Your financial data should inform every major decision you make:

Revenue Analysis

Which products or services generate the most profit? Which customer segments are most valuable? Your bookkeeping data has these answers.

Expense Optimization

Where is your money going? Are there recurring expenses that no longer provide value? Regular financial analysis helps identify waste and optimization opportunities.

Growth Planning

How much cash do you need to scale? What’s your customer acquisition cost? How long is your sales cycle? These metrics come from proper financial tracking.

Building Investor Confidence Through Proper Bookkeeping

If you’re planning to raise funding, your financial records are your business’s report card. Investors want to see:

Clean, organized records that demonstrate you take financial management seriously.

Clear revenue and expense tracking that shows you understand your business model.

Cash flow management that proves you can stretch investment dollars effectively.

Growth metrics that validate your business potential.

Sloppy bookkeeping doesn’t just hurt your chances of getting funded. It suggests you might not be ready for the responsibility of managing investor capital and somehow that seems counterproductive to me.

Technology and Automation: Making Bookkeeping Effortless

The future of bookkeeping for startups is automation. Here’s how to leverage technology to minimize manual work:

Bank Feed Integration

Connect your business bank accounts directly to your bookkeeping software. This automatically imports transactions and reduces manual data entry.

Receipt Scanning Apps

Use apps like Dext (formerly Receipt Bank) or Shoeboxed to automatically capture and categorize receipts. Some accounting software includes this functionality built-in, like afore-mentioned QBO which provides receipt storage functionality through their mobile app.

Recurring Transaction Automation

Set up automatic categorization for recurring expenses like rent, software subscriptions, and loan payments.

Integration with Other Business Tools

Connect your bookkeeping software with your invoicing system, payroll provider, and e-commerce platform to create a seamless financial ecosystem.

Planning for Growth and Scalability

Your bookkeeping system should grow with your business. Here’s how to build for scalability:

Chart of Accounts Design

Start with a simple but expandable chart of accounts. You can always add more categories later, but reorganizing becomes painful as you accumulate data.

Process Documentation

Document your bookkeeping processes so they can be easily handed off to team members or service providers as you grow.

Regular System Reviews

Quarterly, assess whether your current bookkeeping setup still meets your business needs. Growing companies often outgrow their initial systems.

The Bottom Line: Your Financial Foundation Matters

Here’s what I want you to remember from this deep dive into bookkeeping for startups: your financial foundation isn’t sexy, but it’s absolutely critical to your success.

Every successful startup I’ve worked with had one thing in common; they treated financial management as a core business competency, not an afterthought. They understood that proper bookkeeping isn’t about keeping perfect records; it’s about having the financial information necessary to make better business decisions faster.

The entrepreneurs who struggle? They’re usually brilliant at product development or marketing but treat bookkeeping like an afterthought. By the time they realize their mistake, they’re already so far behind the eight ball that difficult and expensive to get caught up.

Don’t be that founder.

Start with the basics: separate business and personal finances, choose the right accounting software, and establish consistent record-keeping habits. As your business grows, invest in professional help and better systems.

Your future self, the one closing that venture capital funding deal or celebrating your first profitable quarter, will thank you for building this foundation today.

Remember, bookkeeping for startups isn’t about perfection; it’s about having enough financial clarity to make informed decisions. Start where you are, use what you have, and improve as you grow.

Ready to take action? Pick one thing from this guide and implement it this week. Whether that’s opening a business bank account, signing up for bookkeeping software, or just organizing last month’s receipts, momentum is more important than perfection.

Your startup’s financial success starts with a single step. Make it count.

About the Author: This guide combines practical experience from working with startups with insights from leading financial professionals. For more startup financial tips and resources, bookmark this page and share it with fellow entrepreneurs who need to get their financial house in order.